finanzmarktwelt – Ihr Auge im Zentrum der Finanzen

Chartanalyse Aktienindizes: Auf was zielt der Markt?

Kommentar - kurz und knapp Aktienmärkte, Gold, Öl seit 2 Tagen ohne Richtung – ein Gedankengang

Aktuell: Öl-Lagerbestände +2,7 Mio Barrels (jetzt 460,0 Mio)

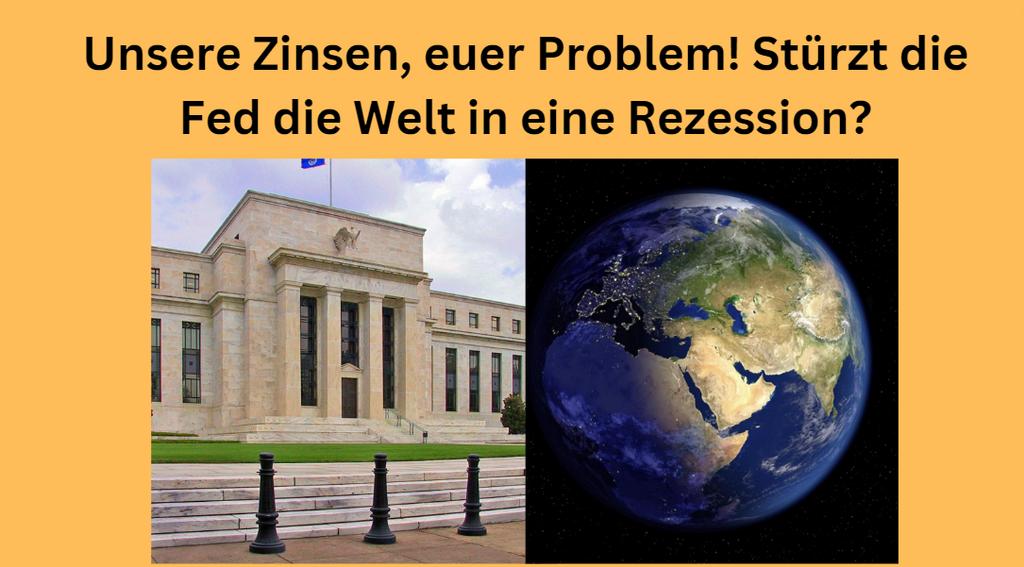

Unsere Zinsen - euer Problem.. Powell-Aussagen zu Zinsen sind Problem für die „Rest-Welt“

Markus Koch LIVE – Überwiegend negative Reaktionen auf Ergebnisse

EU-Pläne Einlagensicherung vergemeinschaften: Sparkassen und Genossen laufen Sturm!

Nvidia-Aktie: Quartalszahlen bringen Schub? Blick auf Erwartungen

Panama-Kanal: Erst 2025 mit voller Kapazität

Meist gelesen 7 Tage

Neue Herausforderungen für Miner Bitcoin-Halving wird den Krypto-Minern einen Schlag verpassen

Zeit für eine Gold-Korrektur? Warum der Goldpreis trotz der Eskalation im Nahen Osten fällt

Wiederholt sich der Nickel-Schock von 2022? Neue Russland-Sanktionen: Aluminium, Nickel steigen sprunghaft

Eskalation im Nahen Osten Bitcoin-Absturz wegen Iran-Angriff – Ein Warnsignal für die Märkte

Ausblick bis Jahresende Zinsen senken – Großbanken sehen nur noch 3 EZB-Schritte

Crash binnen 3 Monaten wegen Fed Black-Monday-Risiko: Fonds hortet zwei Drittel der Anlegergelder in Cash

Goldpreis soll auf 3.000 Dollar steigen laut Citi – aktuelle Aussagen

Rheinmetall-Aktie: KGV soll bis 2026 auf 15 sinken

Unsere Zinsen - euer Problem.. Powell-Aussagen zu Zinsen sind Problem für die „Rest-Welt“

aktien

Chip-Aktien fallen in technische Korrektur

Der Philadelphia Semiconductor Index und Nvidia Corp., ein globaler Indikator für Chip-Aktien, sind zusammen in eine technische Korrektur gefallen, was…

Nvidia-Aktie: Quartalszahlen bringen Schub? Blick auf Erwartungen

TSMC ist günstig bewertet. Nvidia ist vom KGV her spürbar teurer - hier ein Blick auf die Erwartungen vier Wochen…

Europas wertvollste Tech-Firma ASML-Aktie stürzt ab – große Enttäuschung bei Auftragseingängen

ASML meldet heute früh Auftragseingänge, die deutlich unterhalb der Analystenerwartung liegen. China-Exporte sind ein Problem.

Allgemein

Panama-Kanal: Erst 2025 mit voller Kapazität

Der Panama-Kanal, eine der wichtigsten Wasserstraßen der Welt, soll er erst im Jahr 2025 wieder zur vollen Kapazität zurückkehren, nachdem…

GDPNow-Indikator US-Wirtschaftswachstum: Fed-Schätzung steigt auf 2,9 %

Die GDPNow-Schätzung der Atlanta Fed für das US-Wirtschaftswachstum für das erste Quartal steigt annualisiert von 2,8 % auf 2,9 %.

Fed kann Zinsen „so lange wie nötig“ hoch halten, mahnt Powell

Der Enthusiasmus an den Märkten, dass die Zinsen bald und schnell sinken, ist längst verflogen. Die Marktteilnehmer rechnen frühstens mit…

Rohstoffe

Aktuell: Öl-Lagerbestände +2,7 Mio Barrels (jetzt 460,0 Mio)

Die wöchentlich vermeldeten Öl-Lagerbestände in den USA (Rohöl) wurden soeben mit 460,0 Millionen Barrels veröffentlicht. Dies ist im Vergleich zur…

Israel vor Angriff gegen den Iran Ölpreis vor massivem Anstieg? Rekordumsatz bei Call-Optionen

Der Handel mit Call-Optionen auf den Ölpreis erreicht ein Rekordhoch, da der israelische Angriff auf den Iran bald starten könnte.

Wiederholt sich der Nickel-Schock von 2022? Neue Russland-Sanktionen: Aluminium, Nickel steigen sprunghaft

Aluminium mit größtem Anstieg seit 1987

Indizes

Richtungsentscheidung steht an Dax-Erholung stockt: Geopolitisches Risiko im Nahen Osten bremst

Der Dax hat zur Wochenmitte einen zaghaften Erholungsversuch eingeleitet, nachdem die Anleger zuletzt etwas Luft aus dem überhitzten Leitindex herausgelassen…

Kommentar - kurz und knapp Aktienmärkte, Gold, Öl seit 2 Tagen ohne Richtung – ein Gedankengang

Aktuell wirken die Aktienmärkte, aber auch Gold und Öl richtungslos. Es könnte das Abwarten vor dem israelischen Angriff auf den…

Markus Koch LIVE – Überwiegend negative Reaktionen auf Ergebnisse

Markus Koch meldet sich LIVE vor dem Handelsstart in New York. Auf aktuell vermeldete Quartalszahlen wird überwiegend negativ reagiert. Watch…

Konjunkturdaten

Aktuelle Lage der deutschen Wirtschaft weiter schwach ZEW Index besser: Viel Hoffnung, aber wenig Realität

Jeden Monat wird der ZEW-Index vom Mannheimer Zentrum für Europäische Wirtschaftsforschung erhoben – der Index gilt als ein wichtiger Frühindikator…

US-Renditen und Dollar steigen deutlich USA: Einzelhandelsumsatz besser, New York Empire schwächer

Soeben die US-Einzelhandelsumsätze für den Monat März veröffentlicht: Sie sind im Monatsvergleich mit +0,7 Prozent besser als erwartet ausgefallen (Prognose…

US-Verbrauchervertrauen leicht schwächer, Erwartung zur Inflation steigt

Das US-Verbrauchervertrauen der Uni Michigan (1. Veröffentlichung für April), das stark beachtet wird vor allem wegen der Erwartungen der Konsumenten…

Aktien

Höhere Umsatzerwartung für aktuelles Quartal TSMC übertrifft aktuell mit seinen Quartalszahlen die Erwartungen

Die Taiwan Semiconductor Manufacturing Co (TSMC) hat vor wenigen Minuten ihre Quartalszahlen veröffentlicht. Das Unternehmen verzeichnete den ersten Gewinnanstieg seit…

Chip-Aktien fallen in technische Korrektur

Der Philadelphia Semiconductor Index und Nvidia Corp., ein globaler Indikator für Chip-Aktien, sind zusammen in eine technische Korrektur gefallen, was…

Nvidia-Aktie: Quartalszahlen bringen Schub? Blick auf Erwartungen

TSMC ist günstig bewertet. Nvidia ist vom KGV her spürbar teurer - hier ein Blick auf die Erwartungen vier Wochen…

kryptowaehrungen

Marktkapitalisierung erreicht 55% Bitcoin-Dominanz am Kryptomarkt steigt wegen der Spot-ETFs

Die Einführung der Bitcoin Spot ETFs im Januar hat der bekanntesten Kryptowährung der Welt weiteren Auftrieb verliehen und den Kurs…

Eskalation im Nahen Osten Bitcoin-Absturz wegen Iran-Angriff – Ein Warnsignal für die Märkte

Der Bitcoin hat seine jüngste Talfahrt fortgesetzt und ist am späten Samstagabend auf 60.000 USD abgestürzt, nachdem der Iran einen…

Schlechteste Woche in 2024 Bitcoin-Korrektur: Der Abverkauf ist laut Experten nicht zu Ende

Der Bitcoin-Kurs erlebte eine scharfe Korrektur nach dem Erreichen eines neuen Rekordhochs. Ein Grund für den jüngsten Abverkauf findet sich…

Panama-Kanal: Erst 2025 mit voller Kapazität

Der Panama-Kanal, eine der wichtigsten Wasserstraßen der Welt, soll er erst im Jahr 2025 wieder zur vollen Kapazität zurückkehren, nachdem er aufgrund des beispiellosen Wassermangels seine Kapazität in den letzten…

EU-Regularien erhöhen Unsicherheit Immobilien: DWS warnt vor Bewertungs-Risiken in Abwärtsspirale

"Achterbahnfahrt neuer Vorschriften"

GDPNow-Indikator US-Wirtschaftswachstum: Fed-Schätzung steigt auf 2,9 %

Die GDPNow-Schätzung der Atlanta Fed für das US-Wirtschaftswachstum für das erste Quartal steigt annualisiert von 2,8 % auf 2,9 %.